Casey Handmer Feb 2 2022 (original post)

Cheaper hydrocarbons from CO2 direct air capture and sunlight.

Executive Summary

Terraform Industries is a bet on cheap solar, synthetic hydrocarbon supremacy, and hyperscale.

The overarching goal is to zero out the net transport of carbon from the crust to the atmosphere and oceans as quickly as possible by displacing drilled natural gas production with direct atmospheric processing.

As solar power gets cheaper and oil becomes more scarce, at some point this decade it will be cheaper to extract carbon from the air than to drill mile-deep holes in the crust on the other side of the world.

Synthetic fuels are fully backwards compatible with existing infrastructure and usage modalities.

Motivation

In 2022 oil is scarce, atmospheric CO2 levels are rising, and solar energy continues to decline in cost. Indeed, the efficiency of converting natural gas to electricity is about 40%, the efficiency of converting electricity back to natural gas (experimentally) is perhaps 30%. There will come a time, sometime this decade in most places, when it is cheaper to get hydrocarbons by capturing atmospheric CO2 than by drilling a hole in the ground.

The 2020s are poised to see the explosive growth of electrofuels rapidly displacing conventional fossil hydrocarbon production. Electrofuels are burnable fossil fuel substitutes synthesized from chemical precursors using electricity, ideally from renewable sources. Production could exceed 1 GT/year by 2030, with corresponding revenues exceeding $600b.

Economics

Solar electrofuel cost will undercut local hydrocarbon production/importation costs across a steadily increasing fraction of global markets. Terraform Industries is positioned to provide the machinery and logistics to build local capacity to serve this need.

We seek to maximize growth, which means our technical solution needs to be fast, scalable and cheap. While conventional atmospheric processing machinery designs reflect historical energy scarcity and favor energy efficiency over low capex, we take the opposite approach. Our machinery is designed to be cheap enough to internally generate the cash flow needed to finance further growth without excessive reliance on government subsidies or trillion-dollar financing.

Our analysis indicates that capex target costs of $100/T-year and opex target costs of $100/T for CO2 conversion are highly competitive with oil/gas production for any market not directly adjacent to fossil fuel production areas. That is, a plant that captures one thousand tonnes of CO2 per year would cost $100,000 to build, and an additional $100,000 per year to operate. This compares favorably with both solar photovoltaic plant and fracking well economics, meaning that it doesn’t add marginal financing complexity to the former and meaningfully competes with the latter.

We seek to catalyze major growth in this industry. As the market matures, dozens of future market entrants will be our future competitors, suppliers, and customers.

Historical context

Prior to 1913, ammonia was derived from guano and Chilean saltpeter. Subsequently, the Haber process has been used to directly fix nitrogen from the air. The Haber process revolutionized access to ammonia and nitrates, changing the course of industry, agriculture, and war.

Ancient forests and swamps that avoided biological decay were buried and, over millions of years, a small fraction of them were chemically converted to coal, oil, and gas, and then trapped underground in places convenient to 20th century extraction technology.

When people in Britain c. 1800 needed a source of fuel that was less scarce than lumber for metallurgy and primitive steam engines, they turned to coal – a plentiful source of reduced carbon not yet in chemical equilibrium with Earth’s oxidising atmosphere due to its isolation underground. The industrial revolution accelerated human exploitation of fossil carbon, bringing about enormous social and economic changes, tripling the average life span, and also gradually warming the planet via increased atmospheric CO2. Since the beginning of the industrial revolution, humans have extracted and burned about 400 billion tonnes of carbon from the crust, resulting in about 1.5 teratons of additional CO2 in the atmosphere and oceans. In solid form, this could make a mountain significantly taller than Mt Everest. Longer growing seasons and more CO2 have contributed to greater plant growth in regions that aren’t yet too hot, but further warming risks destabilizing ice sheets and flooding our coastal cities.

Chemistry

Combustion is a rapid form of the chemical oxidation reaction, in which “reduced” chemicals or fuels donate electrons to oxygen or some other oxidizer. The Earth’s atmosphere is conveniently 20% oxygen, while chemically reduced carbon is a fundamental building block of life, as shown in the Venn diagram below. This diagram shows fundamental chemical units that combine some subset of carbon, hydrogen, and oxygen.

This transfer of electrons liberates chemical energy as heat, which can boil water or expand gases and be transformed into mechanical work, though never with perfect efficiency.

Photosynthesis is the biochemical reaction in which the energy in sunlight is used to reduce carbon and make it available for plants to grow. This carbon is typically combined with water to form (CH2O)n and other polymers based on “sugars”.

The combustion chemical reaction is reversible. Oxygen is electrically stripped off water molecules, releasing a stream of pure hydrogen. CO2 is concentrated from ambient 410 parts per million to nearly 100% pure. Hydrogen and CO2 are catalytically converted to methane and steam, regenerating water and producing a useful fuel that is backwards compatible with existing infrastructure. While the grid and vehicles will continue their transition to solar and batteries, hydrocarbons will continue to be needed for aircraft, rockets, heating, industry, and chemical manufacturing.

Reversing combustion to generate newly reduced carbon fuel is an energy intensive process, and not even a particularly energy efficient one. But modern solar PV technology is perhaps 1000x better at converting sunlight into useful mechanical work than growing trees and burning them in steam engines, so allowances can be made, and electric fuel synthesis can close both technically and economically.

Market review

Terraform Industries’ design philosophy is to minimize complexity in order to maximize cash flow.

Existing carbon capture approaches fall into two categories. Either they assume someone will print a trillion dollars a year to finance their ongoing operations capturing CO2 and somehow disposing of it, and/or they assume that electricity is expensive and not getting cheaper. Expensive electricity requires highly complex, highly energy efficient processes, which must be financed on infrastructure terms, with 30 year loans to pay off the capital expense of construction.

While these loans serve an important purpose for serving predictable, well defined market needs, they are ill-suited to catalyze the explosive growth of the synthetic fuel industry. If revenue can cover capex in under 12 months, the financial side of the hardware build out has more in common with a Bitcoin mining rig than a petrochemicals plant, and the industry as a whole can scale more rapidly without relying on expensive, scarce long term infrastructure development loans.

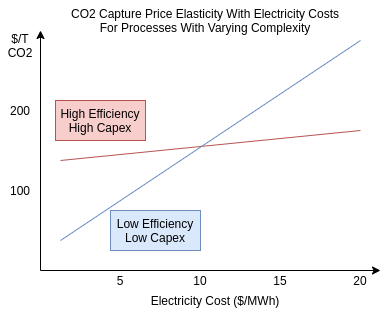

Terraform Industries (TI) seeks to enter the market towards the left of the capex/opex chart above, embodying a process with both competitive production prices and fast scaling potential. When solar PV electricity reaches costs of $5/MWh mid decade, TI’s process will be the first in that market segment.

Falling solar costs demand a low capex approach

Solar costs have fallen with inexorable consistency as manufacturing continues to ramp up. For two decades, cost stabilization has been wrongly predicted to be just around the corner. There is no technically sound reason to suspect that gains will slow, or indeed even cease to accelerate.

At present rates of 10%/year cost reduction, some markets will see $5/MWh at utility scale by 2026, which is not far away. Supply chain difficulties in 2021 slowed this rate slightly, but also greatly increased the cost of natural gas worldwide. If gains continue, by 2036, this price will have been passed worldwide.

Such continuing reductions in solar PV costs could only be driven by explosive growth in demand, over and above that required to saturate demand from traditional electric grids and even electric vehicle charging. TI’s synthetic fuels are poised to generate this demand for electricity.

Indeed, the quantity of electricity required to synthesize 100% of California’s natural gas demand exceeds grid consumption by more than 10:1. This means that synthetic fuel price parity will drive enormous increases in demand for solar power deployment, providing the demand necessary to keep the learning curve bending downwards.

As an aside, scaling production to this demand will result in further price drops for solar power, catalysing other power intensive industries such as atomic recycling and ultimately even mass desalination for agriculture in river basins parched by glacial melt and shifting rainfall patterns.

Synthetic fuel production is enormously energy intensive. One kilogram of synthetic natural gas embodies 55.5 MJ of energy, but more like 150 MJ will have been expended to synthesize it, mostly on hydrogen electrolysis. This may seem wasteful but remember that renewable electricity is cheap and getting cheaper. In terms of opex, electricity is the single greatest factor of production, and yet its cost is reducing by around 10% per year. How can the other factors of production, including parts and labor, possibly match this improvement in cost, year after year? Only by seeking maximal simplicity of design and construction.

Consider the marginal cost elasticity with electricity price for simple and complex processes, shown at right. For higher energy prices, a high complexity system has the lowest overall cost, and costs are relatively insensitive to reductions in energy cost as most of the costs are embodied in the machinery. A simple system is less efficient but better positioned to capture the gains of a reduction in energy cost.

Terraform Industries believes solar prices will continue to plummet and that we will drive and consume much of the next decade of solar supply growth.

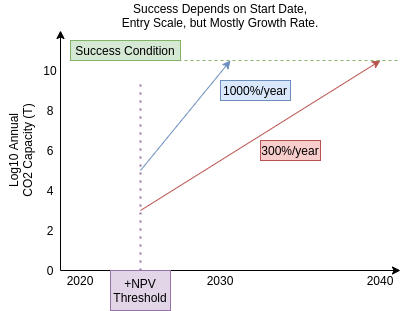

Meeting the success condition depends on start date, entry scale, but mostly growth rate

The success condition is met when the net flow of carbon from the crust to the atmosphere is less than biological fixation rates. At present, this requires displacing or compensating for around 50 GT/year of fossil fuel production.

The continued burning of coal, oil, and gas could be matched by carbon capture with durable storage, but any workable solution has to be able to scale to 50 GT/year, which in addition to acceptably low cost also demands the provisioning of >50 cubic km of volume to store CO2, CaCO3, or some partially reduced bio-oil. As a conical pile of HDPE this would be the tallest mountain in the continental US. Every year.

In contrast, a tonne of synthetic fuel produced is a tonne of crustal carbon extraction displaced, with unmined coal, oil, and gas remaining safely in the crust.

A higher efficiency synthetic fuel approach could reach positive net present value (NPV) as early as 2022, but high implementation costs can slow the growth rate in the absence of sufficient project capital. If implementation costs are around $1000/T-year, reaching 50 GT/year production will require a capital investment of $50t ($5e13), a not insubstantial sum, to be paid off over some decades.

In contrast, Terraform Industries’ lower efficiency synthetic fuel plant may not reach positive NPV until 2026, but once there can scale more quickly as its $100/T-year capex cost can be self-funded through revenue in, at most, a few years of operations. Terraform Industries’ approach leverages cement processing technology so it can hit the ground running with a scale of millions of tonnes per year so it only (only…) needs to achieve four orders of magnitude of growth to reach the success condition. Not easy, but not as hard as, eg, churning out 100 million containerized fuel factories over a similar time scale, and certainly not forbidden by the laws of physics.

The higher the growth rate, the less the scale of the initial condition or the start date matters. At 1000% annual growth, starting at 10,000 T/year instead of 1,000,000 T/year costs two years at the success condition. At a still impressive 300% annual rate, starting small costs twice as long.

Provided that revenue from fuel sales, which is set initially by marginal supply from traditional gas wells, exceeds costs of production, the operation is in the black and, potentially, further complexity can be stripped from the process as the plant design is iterated.

Efficiency gains are incremental and linear. Cost reduction gains drive growth and compound exponentially. Maximal growth rate demands minimal complexity.

Technical approach

Terraform Industries’ fuel production method has three parts: CO2 concentration, green hydrogen production, and fuel synthesis.

CO2 concentration

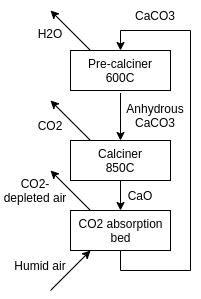

CO2 concentration is performed using a closed lime/calcite calcination cycle, operating at ambient temperature and pressure. CaCO3’s higher calcination temperature means this is roughly 10x as energy intensive as amines (submarines) or zeolites (space stations), but the capture material (lime) is <$10/T, not $2000/T (and up!), in accordance with our low capex/complexity design philosophy. No esoteric materials or catalysts are required. There are essentially infinite, flexible fungible supply chains for all component parts which serve the global cement industry, except for the electric calcination system. Electric calcination is in active development within the cement industry and, being similar to an electrical ceramic kiln, is not mechanically complex.

Cement plants, like the Holcim plant in Ste Genevieve, produce around 5 MT of cement a year. Worldwide cement production is around 5 GT, with half in China, and much from plants which are somewhat smaller. 5 MT of CO2 converted to methane per year implies a plant on a similar scale, albeit surrounded by solar panels, and a production rate well matched to existing natural gas transportation pipeline capacity. A few thousand such plants worldwide, each serving a major city, represents the instantiation of the success condition.

The CO2 concentration cycle begins with electric calcination of limestone/calcite.

CaCO3 -> CaO + CO2 (calcination proceeds quickly at 800-900 C)

The resulting lime (CaO) is fed humid air through a fluidized bed, resulting in the reformation of calcite via the intermediate step of calcium hydroxide (slaked lime).

CaO (s) + H2O (g) -> Ca(OH)2 (S)

Ca(OH)2 (s) + CO2 (g) -> CaCO3 (s) + H2O (g)

The result is a mixture of CaO, Ca(OH)2, and CaCO3, with absorption of CO2 slowing as more CaCO3 forms and the bed saturates.

The resulting powder is fed into an electric kiln first to dehydrate it at up to 600 C, then back into the 850 C kiln to complete calcination.

CaO + Ca(OH)2 + CaCO3 -> CaO + CaCO3 + H2O (g) (400 C < T < 600 C)

This cycle can be performed with continuous or batch material processing machinery, increasing development options and reducing cost. CO2 fixation and separation are separate processes, so the concentrated CO2 stream can be modulated in real time to match demand.

Green hydrogen

Commercial lab-grade electrolysis machines cost >$10,000/kW, and perform at up to 84% efficiency. They are expensive because they’re stainless steel pressure vessels that perform electrolysis on a superheated, super pressurized, super alkaline fluid that is a lawsuit waiting to happen. Supercritical lye is not a friendly chemical.

Hydrogen generated using water and renewable electricity (green hydrogen) has traditionally been more expensive than hydrogen generated by steam reformation of natural gas (gray hydrogen). This gap is closing as billions are invested in hydrogen electrolysis technology, derisking this part of TI’s process.

Terraform Industries prototype low cost electrolysis cells are $20/kW and achieve 40% efficiency. They are an atmospheric pressure, low efficiency system utilizing 26% w/w KOH alkaline solution and graphite electrodes, most of which are passive and in series. Full scale production calls for 1 MW cells at pallet scale, distributed between solar panel units in place of the usual solar farm inverters, venting waste oxygen directly, and transporting hydrogen in ambient pressure, large diameter plastic tubes.

Chemically, the electrolysis reaction is

2H2O (l) -> 2H2 (g) + O2 (g)

This reaction would consume 142 MJ of electricity per kilogram of H2 produced at 100% efficiency. TI targets around 600 MJ/kg to exploit the relatively low cost of electricity compared with electrolysis cell capital expenditure.

Fuel Synthesis

Hydrogen, as a fuel, is marginal even for rockets. It’s not backwards compatible with our existing industrial stack. It’s quite difficult to work with and to transport. It leaks through metals, embrittles materials, and has amazingly low density. Zeppelins, maybe. As fuel? TI does not expect to see it gaining traction.

Similarly, capturing CO2 is fine but what then? It’s unreactive, as dense as hydrogen is sparse, and not particularly valuable. It’s also hard to store or transport.

After CO2 concentration and hydrogen production, TI has a whole bunch of both streaming from pipes. The approach is to avoid transport and storage by immediately reacting the hydrogen with captured CO2 to produce methane (CH4). This is a similar in principle to avoiding the hazards of sodium and chlorine gas by storing them together as common table salt (NaCl).

By analogy with the traditional combustion reaction:

CH4 + 2O2 -> CO2 + 2H2O ΔH = -890.8 kJ/mol

The Sabatier reaction reduces CO2 by burning it in pure hydrogen:

4H2 + CO2 <-> 2H2O + CH4 (nickel/alumina catalyst) ΔH = -165 kJ/mol.

While the reaction does not run to completion, the unwanted reaction products are easy enough to remove from the exit stream. Combined with the electrolysis step, the complete reaction is:

4H2O + CO2 -> 2O2 + 2H2O + CH4

The only waste products are oxygen and water vapor.

The Sabatier reaction was discovered in 1897. It is not particularly exotic or difficult to execute. The resulting methane can be upgraded to long chain hydrocarbons, such as gasoline, using the Fischer-Tropsch reaction. This process has been implemented at industrial scale numerous times, including at the Oryx plant pictured below.

Summary

The Terraform Industries synthetic fuel plant takes as inputs copious solar power (DC, high current) and air, and produces natural gas, with waste products of oxygen and distilled water. The per-Watt cost is lower than the solar PV arrays it ultimately depends on, ensuring that solar PV cost remains on the critical path for however long the price continues to fall. We expect to hit cost parity without subsidies, tariffs, or curtailment in limited markets by 2025. If historical solar production increases continue, we should be able to serve half the world’s population by the early 2030s and the rest by 2040.

What does the world energy mix look like in 2040? Mostly solar, some wind, nuclear, hydro, and very limited legacy fossil fuels. Many cars, buses, trucks, buildings are run with electricity. Local battery storage continues to grow as market needs require. Grids are run mostly at the local level. Hydrocarbon use in general reduces even as prices drop (electricity is cheaper still), while usage tends towards shorter chains and lighter fractions. Synthetic production of hydrocarbons is cheaper than fossil extraction and refining nearly everywhere. Cheaper energy means cheaper, faster aviation, bigger and cleaner industry, better recycling, and renewed local manufacturing worldwide. By 2040, solar costs are so low that mass desalination can begin to compensate for unpredictable rainfall patterns – but that’s another story.

Strategy

- De-risk CO2 concentration by building development plants at up to 500 kg/day scale, with an initial cost target of $100/T-year.

- Build a low cost development green hydrogen plant.

- Synthesize methane, qualify end-to-end production and assay process.

- Execute large scale plant including the solar farm with colocated machinery, proximal to existing natural gas distribution pipeline, and with customer agreements.

- Scale plant production by all available means. Target commissioning of one MT-scale plant per day within five years of market entry.

Questions

Tree. You’ve invented a tree.

As far as rapidly self-scaling solar-powered carbon reduction machines go, plants have been at it for a long long time. Indeed, coal, oil, and gas is the result of a very lossy and time consuming process whereby humans burn, in a single day, solar energy that was stored over thousands of years.

Alternatively, biofuel production from, eg, corn, can be considered carbon neutral if one ignores the carbon intensity of farming and fuel transport. However, there is a limit to how much corn can be grown, determined by water, climate, and land area. Even corn, with incredible C4 photosynthesis, fixes less carbon on an area-annual basis, than a quarter-inch layer of dry lime. The end-to-end efficiency per solar photon for biofuels is <0.1%, while PV+batteries+motors can be as high as 20%. Synthetic fuels are around 5% efficient, which is still a 50x better use of land than growing corn, and can be done in arid regions.

Is that like Prometheus Fuels?

Prometheus Fuels’ business plan is premised on the same observation: cheap solar will result in cheaper synthetic fuel than stuff extracted from the crust. Their website is also impossibly cool.

Prometheus uses aqueous chemistry and a very clever nano-filtration system to separate alcohols without fractional distillation.

Terraform Industries’ approach is deliberately simpler, cheaper, and less capital intensive. Wherever solar is cheap enough, TI can potentially scale more quickly. But TI believes that the world is big enough for two, or two hundred, solar synthetic fuel companies.

TI’s strategy is to stake out the cheap, fast corner of the market. We openly encourage competitors but if a more complex technology faces scaling limitations, TI is the backstop.

Could China steal IP?

When it comes to ensuring strategic access to hydrocarbons, China will not be the odd country out for ignoring international IP agreements and infringing as much as possible. So how can Terraform Industries prevent Chinese, or any international, competition?

For Terraform Industries, achieving the success condition through total verticalization and monopolization of the synthetic fuels industry is sub-optimal. We believe that a better, faster solution will be found through the massively parallel development of competing and complementary synthetic fuel technologies. We believe that the first mover advantage lies with companies that invest their resources in growth and market making, not patent squatting.

The odds of the early generations of technology being defensible from an IP standpoint, or even worth defending, is extremely low. Terraform believes that following six month design cycles common in solar PV, we would consider ourselves lucky to get to the success condition by version 10, or even version 20, of the complete tech stack.

Indeed, given the rarity of synthetic fuel plays that capitalize on cheap solar, we would be gratified to see competitors follow us into this market. And if Chinese manufacturers can make CO2 concentrators, electrolysis units, or Sabatier reactors cheaply and in enough abundance to saturate domestic Chinese demand with product left over, we would be fortunate to partner with them as suppliers!

Team

Casey Handmer PhD. Casey earned his PhD in gravitational wave simulation from Caltech in 2015. He designed maglev systems at Hyperloop and built GPS science instruments and mapping tools at NASA JPL before founding Terraform Industries.

David Smyth worked on software for the Space Shuttle and JPL Mars rovers, before stints at Millennium Space Systems and Honeybee Robotics. He’s also the President of Westlawn Institute of Marine Technology.

Stephanie Coronel PhD. Stephanie completed her PhD studying mechanics of composite fuel tank ignition prevention at Caltech, followed by work on combustion safety at Boeing and Sandia National Laboratory.

Jenna Amundson brings deep experience with marketing and people ops from Hyperloop and Jenlis.

We’re also proud to work with Second Group Design engineers Brian Towle (GE, Hyperloop) and Jett Ferm (Pilot Group, Hyperloop) to fine tune our carbon filter.

Join us!

Follow along on our website, Twitter, or join our mailing list for updates.

Terraform Industries is hiring! Join us on our mission to yank billions of tonnes of CO2 out of the atmosphere and make money in the process. We’re particularly keen on MechEs, ChemEs, EEs, and anyone else with strong mechanical intuition and fabrication experience. Send us your most compelling one-pager to hiring@terraformindustries.com.

3 thoughts on “Terraform Industries Whitepaper”